When you’re trying to stay on top of your credit score, it can feel like a game of whack-a-mole. Every time you think you’ve got it figured out, a new app pops up with a different score. Well, that’s exactly what happened to me when I started tracking my credit score on OneScore and PaisaBazaar. The more I dived into the numbers, the more I realized that credit scores on different apps aren’t as straightforward as they seem.

The Story Behind My Credit Score Journey

So here’s the deal. A few months ago, I was happily tracking my credit score on OneScore—an app that seemed pretty reliable. I had a basic understanding of my score, tracked it monthly, and thought I was doing everything right. My credit score was consistently hovering around a decent level, but I wasn’t too concerned. Then, one day, I decided to explore PaisaBazaar to see if there were any “pre-approved” credit card offers.

Imagine my surprise when I not only got access to pre-approved offers but also to my credit reports from CIBIL, Experian, CRIF, and Highmark. Until that point, OneScore had only provided me with CIBIL and Experian. I thought this was a goldmine of information! But soon, I started noticing discrepancies between the credit scores on both apps.

The Curious Case of Two Different Scores

After logging into PaisaBazaar and seeing my scores from different agencies, I couldn’t help but notice something odd. The refresh dates on PB and OneScore were about 15-16 days apart, which I figured could explain minor score differences. But then, something strange happened. The difference in my CIBIL and Experian scores on the two apps started growing.

Here’s a breakdown of what I saw:

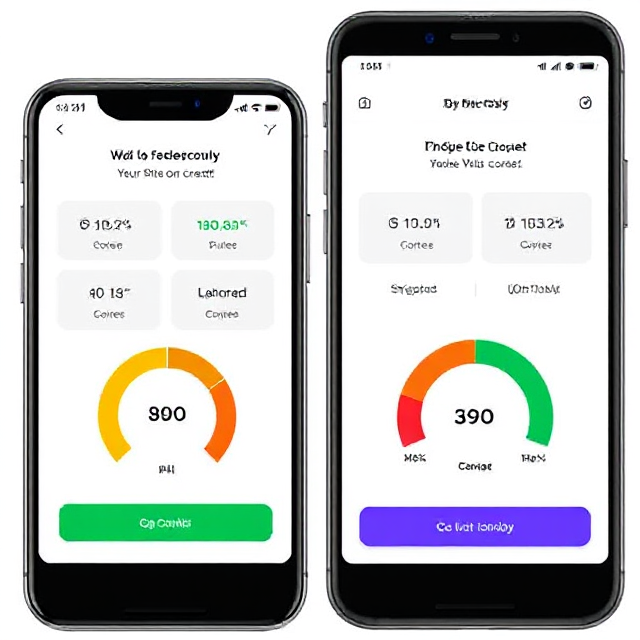

- OneScore:

- CIBIL: 755 (Updated today, up by 3 points from last month)

- Experian: 861 (Updated 16 days ago, up by 32 points from last month)

- PaisaBazaar:

- CIBIL: 768 (Updated on 5th April, up by 15 points from last month)

- Experian: 837 (Updated on 26th April, up by 9 points from last month)

Why Are the Scores Different?

If you’ve been in the credit score game long enough, you know that different agencies calculate your credit score based on different criteria. CIBIL and Experian, two of the major credit bureaus in India, use slightly varied methods to assess your creditworthiness.

- CIBIL scores are calculated based on your credit history, outstanding debts, credit utilization, and payment history.

- Experian scores, on the other hand, consider factors like your credit mix, length of credit history, and recent credit inquiries.

Why This Matters

The discrepancies you see on different apps stem from these differences in how the scores are calculated. So, if OneScore and PaisaBazaar are pulling from different bureaus or using slightly different methods to update your scores, you’re bound to see variations. The key takeaway here is that while these scores may differ, they are still offering an accurate representation of your financial health according to their own algorithms.

Which One Should You Trust?

Now, you might be asking yourself: Which score should I trust? Good question! In my experience, PaisaBazaar has been a bit more reliable, at least in terms of Experian. When PaisaBazaar updates my Experian score, I also get an email from Experian itself confirming the update. This makes me feel confident that the PaisaBazaar score is accurate.

However, both apps are offering you valuable insights into your credit profile, so trust them for what they are: tools to help you manage your credit health.

A Side Note on Credit Utilization

One thing that can throw off your scores, no matter which app you use, is credit utilization. When I first started tracking my score, I didn’t realize how important it was to keep my credit utilization under 30%. Back in the day, I thought the more I used my credit and paid it off on time, the better I would look in the eyes of banks. But that’s not the case. High utilization can lower your score even if you’re paying your bills on time.

In fact, since I reduced my utilization to under 30%, I expected a much larger jump in my scores. But that didn’t happen immediately, which just goes to show that credit score improvements take time and depend on multiple factors.

The “Pre-approved” Offer That Made Me Pause

Here’s where things get interesting. A few weeks ago, I received a “pre-approved” offer for a SaveMax Credit Card from BankBazaar and RBL. Out of curiosity, I checked my CIBIL score on their platform and, low and behold, I was “pre-approved.”

I thought, why not? So, I agreed to apply. The agent checked and said the application was already submitted. That was a surprise. And to make things even more bizarre, I haven’t received any further communication from RBL or BankBazaar for 26 days. But when I checked my CIBIL report, I noticed a “CIBIL Inquiry” on the same day I spoke with the agent.

What Does This Mean?

A CIBIL Inquiry isn’t necessarily a bad thing, but it does show that your credit report has been checked by a financial institution. Multiple inquiries can sometimes affect your score, especially if they occur in a short period.

In my case, it seems like the pre-approved offer may have been a little too aggressive, leading to a CIBIL inquiry that might impact my score negatively for a short while.

Should I Apply for the RBL LazyPay Card?

Now, the real question: should I apply for the RBL LazyPay card? If you ask me, I would suggest waiting until the situation with the SaveMax card is resolved. Multiple applications in a short period can affect your score, and since I’m still waiting for clarity on the pre-approved offer, it’s best to hold off on additional credit inquiries for now.

Frequently Asked Questions

Why do I see different credit scores on OneScore and PaisaBazaar?

The difference in credit scores across OneScore and PaisaBazaar can be due to variations in the credit bureaus they use. Each platform may rely on a different credit bureau (such as CIBIL, Experian, or Equifax), which can lead to slight differences in the scoring models and information presented.

Which credit score is more accurate, OneScore or PaisaBazaar?

Both OneScore and PaisaBazaar provide reliable credit scores, but the accuracy depends on the data source used. It’s important to check the credit score from multiple platforms to get a more comprehensive view of your creditworthiness. However, the score from the credit bureau you’re applying for a loan with is typically the one that matters most.

Can the credit score on OneScore or PaisaBazaar impact my loan approval?

While the credit score provided by OneScore or PaisaBazaar is useful for monitoring your credit health, the score that lenders refer to when processing your loan application is typically the one sourced directly from a credit bureau. It’s always a good idea to review your credit score before applying for any loans to ensure it meets the lender’s criteria.

How do OneScore and PaisaBazaar calculate my credit score?

Both OneScore and PaisaBazaar calculate your credit score based on factors like your payment history, credit utilization, length of credit history, and recent credit inquiries. The exact weight given to each factor may vary depending on the credit bureau or model used by each platform.

Can I trust the credit scores provided by OneScore and PaisaBazaar?

Yes, you can trust the credit scores provided by OneScore and PaisaBazaar, as they are based on data from reputed credit bureaus. However, since different bureaus may calculate scores differently, it’s important to cross-check and monitor your credit score regularly across multiple platforms to ensure accuracy.

Conclusion

The variation in credit scores between OneScore and PaisaBazaar is primarily due to the different credit bureaus and scoring models each app uses. While both platforms offer valuable insights into your credit health, the score on one app might differ slightly from the other based on how data is processed and the scoring criteria involved. It’s essential to consider these differences and use the scores from both platforms as part of your broader credit monitoring strategy. For loan approvals, always refer to the score provided by the lender’s chosen credit bureau. Regularly checking your credit score on multiple apps helps you stay informed and make better financial decisions.