Today, we’ll discuss how canceling your credit card can negatively affect your CIBIL score and ways to minimize its impact. Before diving into the cancellation process, let’s first explore how credit card cancellation can affect your CIBIL score.

Negative Impact on CIBIL Score:

Reduction in the Number of Credit Accounts

When you close a credit account, it directly affects your CIBIL score as the number of active credit accounts is a key factor. Credit cards and loan accounts fall under this category, and the total number of these accounts influences your score. By closing a credit card, you lose one account, resulting in a decrease in your overall CIBIL score.

Decrease in Overall Credit Limit

Closing a credit account also reduces your total available credit limit. For instance, if you have two credit cards with credit limits of ₹1 Lakh and ₹2 Lakhs, your total credit limit is ₹3 Lakhs. Once you close one card, your available limit decreases, which can negatively impact your CIBIL score. A higher total credit limit is beneficial for maintaining a good score.

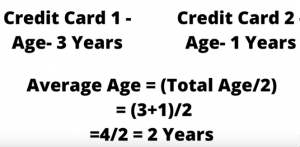

Decline in the Average Age of Credit Accounts

The age of your credit accounts is another important factor in determining your CIBIL score. If you have two credit cards, one being 3 years old and the other 1 year old, your average credit age is (3 + 1) / 2 = 2 years. Closing the older account reduces the average age, bringing it down to 1 year and potentially affecting your score.

What Should You Do If You Have Older Credit Cards with Annual Charges?

If you’re paying yearly charges on an old credit card, consider contacting your bank and requesting them to downgrade the card to a free version. Most banks offer a basic, no-fee credit card, which can help you retain your credit history without the annual charges.

Free Credit Cards from Various Banks:

- ICICI Bank Platinum Chip Credit Card

- AXIS Bank My Zone Credit Card

- You can convert any HDFC Credit Card into a lifetime free card – (Video Guide: https://youtu. be/Bt765ZwvGLk)

- IndusInd Bank Platinum Credit Card, and more.

If you’re paying high annual fees, you can ask your bank to downgrade your card. If they agree, you’ll continue enjoying the same benefits. However, if they refuse, it’s better to close the card rather than paying high maintenance charges. The impact on your CIBIL score will be temporary and will improve over time.

How to Close Your Credit Card:

The process of closing a credit card is generally the same across all banks. Here’s what you need to do:

- Clear All Dues: Ensure you’ve paid off both billed and unbilled amounts.

- Close Any EMI: If you have any outstanding EMIs, settle them by paying the foreclosure charges, as pending EMIs will prevent the cancellation.

- Redeem Your Rewards: Use or redeem any accumulated reward points, whether in cash or via the bank’s preferred method.

Once you’ve completed these steps, you can either:

- Call Customer Care: Request credit card cancellation, and the agent will raise a ticket. The cancellation process usually takes up to three working days.

OR

- Visit the Bank Branch: Fill out the credit card cancellation form, and the process will be completed in three days.

Frequently Asked Questions

How do I cancel my credit card with SBI, HDFC, ICICI, Axis, CITI, or IndusInd?

To cancel your credit card with any of these banks, you need to clear all dues (both billed and unbilled amounts), pay off any outstanding EMIs, and redeem any reward points. Afterward, you can either call customer care or visit the bank branch to request cancellation. The process generally takes 3 working days to complete.

Will canceling my credit card affect my CIBIL score?

Yes, canceling a credit card can have a temporary negative impact on your CIBIL score. This is because it reduces the number of credit accounts and your available credit limit. However, over time, your score will improve as long as you maintain responsible credit behavior on other accounts.

Can I convert my credit card into a lifetime free card instead of canceling it?

Yes, some banks like HDFC allow you to convert certain credit cards into lifetime free cards. If you’re paying high annual fees, you can contact your bank to request this conversion. If they agree, you can continue using the card without any charges. However, if the bank denies the request, closing the card may be a better option.

How long does it take to cancel a credit card with these banks?

Typically, the cancellation process takes up to 3 working days once the bank processes your request. If you’re submitting the request in person at the branch, the process will still take around 3 days to complete.

Can I continue using my credit card after submitting a cancellation request?

No, once you place a cancellation request, avoid using the card for any transactions. If you continue to use the card after the cancellation request, it will invalidate the process, and the cancellation will not be processed further.

Conclusion

Canceling a credit card is a straightforward process that involves settling any dues, closing outstanding EMIs, and redeeming any rewards points. Once these steps are completed, you can either call customer care or visit the bank branch to initiate the cancellation request. While the cancellation process usually takes up to 3 working days, it’s essential to refrain from using the card once the request is submitted to ensure a smooth closure.

However, before canceling your card, it’s important to consider the potential impact on your CIBIL score. Closing a credit card may temporarily reduce your score by lowering your total credit limit and the number of credit accounts. To minimize this, ensure that you maintain responsible credit behavior across other accounts. If high annual charges are a concern, exploring the option of converting your card to a lifetime free version could be a viable alternative.